How to Set Financial Goals

June 29, 2023

Navigating personal finance can be daunting. Without guidance, it’s easy to get lost in unplanned expenses, debt, and missed financial chances. Think of financial goals as your roadmap, guiding your money choices. Whether you want to buy a new house, retire early, or just manage your spending better, it starts with setting financial targets.

Topics Covered: What are Financial Goals? Characteristics of Good Financial Goals Short-term Financial Goals Medium-term Financial Goals Long-term Financial Goals How to Stay on Track with Your Goals What Can CreditU Do For You? Key Insights – Setting Financial Goals

What Are Financial Goals

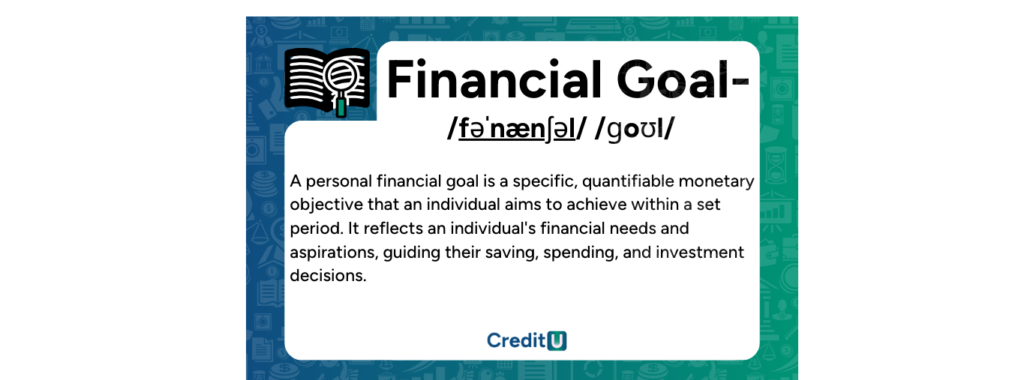

Personal financial goals are specific, quantifiable monetary objective that an individual aims to achieve within a set period. It reflects an individual’s financial needs and aspirations, guiding their saving, spending, and investment decisions. These goals can vary significantly based on an individual’s life stage, values, income, expenses, and broader life goals.

Personal financial goals can be categorized based on their duration:

- Short-Term Goals (1-2 years): These are immediate goals that one aims to achieve in the near future. Examples include saving for a vacation, paying off a specific credit card debt, or building an emergency fund.

- Medium-Term Goals (3-7 years): These are intermediate goals that require a longer horizon for planning and saving. Examples might be saving for a down payment on a house, buying a car, or funding higher education.

- Long-Term Goals (8 years and beyond): These are goals that have a long timeframe and usually revolve around life’s significant milestones and post-retirement plans. Examples include saving for children’s education, achieving financial independence, or building a retirement nest egg.

Your personal finances don’t stop with just earning an income and budgeting. Setting financial goals is also crucial. While we need to pay for our daily living expenses, personal finance isn’t just about spending for your current life. It’s also about using your money to set you up for a life you want to live long-term. When you set financial goals, you’re being intentional with your money, instead of frittering it all away. A good personal financial goal has proper structure and specific characteristics. Let’s look at them in a little more detail.

Characteristics of an Effective Personal Financial Goals

When setting personal financial goals, it’s crucial to ensure they are well-structured to guide your financial journey effectively. An ideal personal financial goal will possess these distinct features:

- Specificity: Your goal needs precision. Ambiguous objectives like “I want to save money” can leave you directionless. Instead, zoom in on the details. For instance, rather than a generic aim, say, “I aim to save $10,000.” This clarity not only provides focus but also drives commitment.

- Measurability: Tracking progress is pivotal to maintaining motivation and ensuring you’re on the right path. For a goal like saving $10,000 over 2 years, a measurable checkpoint would involve ensuring you’ve stashed away $5,000 by the end of the first year. Regular progress checks give you a sense of accomplishment and allow timely adjustments.

- Attainability: While it’s commendable to aim high, it’s also essential to stay grounded in reality. Your financial goals should consider your current resources, future prospects, and potential challenges. Setting wildly unreachable targets can lead to disillusionment. However, a goal that’s challenging yet achievable can be motivating.

- Relevance: Your financial objectives should resonate with your overall life aspirations and core values. For instance, if owning property isn’t a priority for you, setting aside a significant sum for a house down payment might not be the best use of your funds. Tailor your goals to your personal journey and priorities.

- Time-Bound: Every goal needs a deadline. This creates urgency and focus. Instead of an open-ended “I’d like to own a house someday,” zero in on a timeframe like, “I aim to buy a house in the next 5 years.” Time constraints prompt planning, timely action, and often, a more disciplined approach.

To encapsulate, a well-structured personal financial goal acts as a navigational tool. It orients and shapes your financial behaviors and choices, steering you towards your desired financial milestones.

Real life Situation

Mike and Shalini are currently renting an apartment and they are looking to save enough money for a down payment on a new home in the next two years. Here’s how this overall goal can be broken down to be more precise.

1.Specific: They aim to save $50,000 for the down payment.

2.Measurable: They will set aside a specific sum every month and review my savings quarterly. By the end of each year, they should have saved $25,000 to remain on track.

3.Attainable: Based on their current income and monthly expenses, they can reasonably save $2084 each month, which amounts to $25,000 annually. They will also explore additional income streams, such as freelance work, to boost savings if needed.

4.Relevant: Owning a home is important to Mike and Shalini. It aligns with their desire for stability and represents a long-term investment in my financial future. It’s also a milestone they’ve always aspired to achieve by the time they reach 30.

5.Time-Bound: They will aim to buy a new home in 2 years, by September 2025, using the $50,000 they have saved as the down payment.

How To Set Financial Goals – A Comprehensive Guide

In today’s unpredictable economic conditions, having financial clarity can be a source of stability. Financial goals, be it short-term, medium-term, or long-term, can provide the roadmap needed to navigate life’s twists and turns. But how do you set these goals and ensure they align with your overall life plans? Let’s dive in.

The Importance of Financial Goals

Financial goals are the milestones you set to achieve your financial aspirations. They’re the actionable steps that lead to a bigger dream, like buying a home, traveling the world, or achieving financial independence. By defining these goals, you give yourself a clear path forward and make your financial decisions purposeful. It is important that you look at financial goals for the short, medium and the long term in order for it to be a comprehensive picture.

Short-Term Financial Goals (1-2 years)

In the journey of personal finance, short-term goals serve as the stepping stones that pave the way for bigger achievements. They offer quick wins, boost confidence, and provide the foundation for more extensive financial planning. Here’s how you can set actionable short-term financial goals that align with a 1-2 year timeline:

Craft a Comprehensive Budget:

This should be the most important step of financial goal setting. Initiate your financial planning by getting a clear picture of your income and expenses. List down all sources of revenue and all monthly expenses to determine where your money comes from and where it goes. Money Management apps such as CreditU can simplify this task for you. The help these apps provide to categorize your expenses, set budget limits and provide useful insights into your overall finances can be an invaluable asset.

Build an Emergency Fund:

An unforeseen crisis can derail the best-laid plans. That’s why having a safety net is vital. Setting aside money to cover at least 3-6 months of living expenses must be a big part of your short-term financial goal setting. Sudden adversities such as job loss, car repairs or a medical emergency can happen to anyone. Being prepared to tackle these expenses without having to plunge into debt is a part of being financially prepared. Setting this as a short-term financial goals facilitates this preparedness.

Prioritize High-Interest Debt Elimination:

The Pitfalls of High-Interest Debt: Debt, especially those with high interest, can significantly hamper financial growth. The interest accumulates quickly, making the principal harder to clear off. In the short-term one must focus on paying off high-interest debts, like credit card balances or predatory loans, as a priority. The sooner you clear these, the less money you’ll waste on interest, and the quicker you can redirect those funds to other medium and longer-term financial goals.

Anticipate and Save for Upcoming Expenditures:

We all have events or purchases on the horizon we’re excited about, be it a dream vacation, attending a close friend’s wedding, or buying the latest tech gadget. These may be splurges. However, properly planned for, these can be fulfilled. If you are looking forward to a vacation at the end of the year dedicating a savings fund to this goal can ease your financial stress. Instead of resorting to last-minute loans or credit card swipes, forecast these expenses and start a dedicated savings fund. By allocating a specific amount each month, you can comfortably afford these pleasures without jeopardizing your financial health.

By diligently addressing these short-term financial objectives, you lay a robust foundation for your long-term financial dreams. Short-term goals are the significant, initial strides for your next steps. Therefore, spend the time to identify these goals and work towards achieving them.

Medium-Term Financial Goals (3-7 years)

In the journey of personal finance, medium-term goals serve as pivotal milestones that bridge the gap between immediate needs and long-term aspirations. These goals, typically spanning 3-7 years, require a mix of planning, discipline, and foresight. Here’s a deeper dive into some common medium-term financial goals and why they matter:

Building a Robust Emergency Fund:

Your emergency fund is more of a rolling financial goal. Having a robust plan to grow it and strengthen it should always be a part of your plan. Your goal should be to gradually increase your emergency fund to cover anywhere from six months to a full year’s worth of expenses.

An expanded emergency fund offers a safety net against unforeseen financial shocks, be it job loss, medical emergencies, or urgent home repairs. With a substantial buffer, you can navigate challenges without compromising your other financial objectives or sinking into debt. In the medium-term you can automate transfers to your emergency fund to ensure consistency.

Investing in Skill Development:

Personal development should always be a part of your personal finance plan. IN your medium-term financial plan make sure you allocate funds to pursue courses, workshops, or certifications that align with your career goals.

Continual learning can propel you ahead in your professional journey. By acquiring new skills or refining existing ones, you enhance your employability, open doors to higher-paying opportunities, and potentially achieve job security.

Research courses or qualifications that are in demand in your industry. Budget for these expenses and consider them an investment in your future earning potential.

Secure your loved ones:

If you have family members like a spouse or children relying on your income, it’s essential to consider life insurance. This ensures they’re financially protected should you pass away unexpectedly. Term life insurance is a straightforward and cost-effective choice for many, covering most individual insurance requirements. Consulting with an insurance broker can help you navigate and find a policy tailored to your needs. Although most term life insurance policies involve medical evaluations, many people can secure a policy unless they have severe health conditions.

Moreover, disability insurance is a vital safeguard to maintain your income stream during your working years. While many employers offer this coverage as part of their benefits package, those without this perk should consider securing a policy independently, effective up to the age of retirement.

The main benefit of disability insurance is its ability to substitute a significant fraction of your earnings if a severe illness or injury prevents you from working. Often, this insurance provides a more substantial payout than what Social Security disability income offers. This added financial cushion can ensure a more comfortable living standard for you and your family during challenging times. It’s worth noting there’s typically a gap between the onset of your disability and the commencement of insurance payouts. This potential delay underscores the importance of maintaining an emergency fund as a financial safety net.

Medium-term financial goals are more than just future expenditures; they represent your evolving aspirations, priorities, and life stages. By setting and working towards these objectives, you ensure that your financial journey is both rewarding and aligned with your life’s vision.

Long-Term Financial Goals (8 Years or More)

When you project a financial path spanning 8 years or more, you’re essentially laying a foundation for significant life events and milestones. Long-term financial planning demands both foresight and patience. Here’s a closer look at some primary long-term objectives you might consider:

Retirement Savings – The Earlier, The Better:

While retirement might seem a distant reality, starting early can reap substantial rewards, thanks to compound interest. The power of compounding can turn even modest regular contributions into a sizeable nest egg over time. Tax-advantaged accounts like 401(k)s or IRAs are excellent vehicles for retirement savings. Not only do they provide potential tax savings now, but they can also lead to significant growth over time. To ascertain the amount you’ll need, start by estimating your desired annual retirement income. Factor in potential pensions, social security, and other income sources. From there, calculate the necessary monthly contributions to reach your target.

Pay off your mortgage:

In the long-term, paying off your mortgage early can lead to thousands saved in interest payments. This step can also free up a significant portion of your monthly budget. Consider making biweekly payments or adding an extra monthly payment annually. Even a slight increase in your monthly contribution can shorten the lifespan of your loan. Planning for this goal can help you ease the stress in your retirement years.

Planning for Education:

If you have children in the financial picture, higher education can be a considerable expense. However, there are many tools to help you plan for this goal. Higher education can be a substantial expense, but starting a college fund early can ease this burden. You’re not just saving; you’re investing in the future. Tax-advantaged savings options, like 529 plans, can offer both growth and tax benefits. These plans allow your investments to grow tax-free, provided they’re used for qualified educational expenses.

Embarking on the journey of setting long-term financial goals can feel daunting. But with clarity, consistency, and commitment, these visions can translate into tangible realities, ensuring a more secure and enriched future.

Tips to Stay On Track

To ensure that you’re consistently progressing towards your financial goals, it’s imperative to employ proactive strategies. As with any journey, obstacles and detours can arise; being prepared helps you navigate them effectively. Here’s an expanded guide on maintaining your financial momentum:

Annual Financial Check-ups:

Just as our lives evolve, so do our financial realities. What may have been a priority one year might shift the next. Regular check-ins ensure that your goals align with your current situation.

Set aside a specific time annually. Perhaps at the beginning of the year or on your birthday to assess your financial health. Examine your savings, debt, investments, and other financial parameters. Adjust your strategies accordingly to stay aligned with your goals.

Stay Financially Literate:

Financial markets can be volatile. Interest rates fluctuate, and global economic scenarios can shift, impacting your investments and savings strategies.

Dedicate some time each week to read financial news, attend webinars, or even take online courses. Knowledge equips you to adapt and make well-informed decisions in a dynamic environment.

Harness Professional Expertise:

The world of finance can be complex, and individual needs vary. An expert can offer insights tailored specifically to your situation.

Consider consulting a financial planner or a professional financial counselor. These professionals can assess your overall financial health, clarify your goals, and craft strategies that optimize your assets and earnings. They bring a wealth of knowledge and can be particularly beneficial if you’re navigating complicated financial scenarios.

The Virtue of Financial Patience:

While it’s exciting to reach financial milestones, the journey is often longer than anticipated. It’s essential to understand that wealth-building is typically a slow and steady process.

Resist the urge to seek quick fixes or jump on every financial fad. Instead, embrace patience and discipline. Celebrate small victories along the way and remember that consistent effort and a clear vision will ultimately lead you to your financial destinations.

In essence, your financial journey is a dynamic one, influenced by both personal changes and broader economic shifts. Staying vigilant, informed, and patient will ensure you remain on a trajectory towards success.

What Can CreditU Do For You?

Get ready to rule your finances like a pro without lifting a finger! Introducing CreditU – the ultimate personal finance tool that helps you plan budgets, sync bank and credit card accounts, and even track your financial goals. CreditU even offers personalized financial education tailored for your specific financial situation.

Setting financial goals is one of the most important steps towards achieving financial stability. Without a clear plan in place, it’s easy to fall into the trap of overspending and accumulating debt. By using a tool like CreditU, you can create realistic and achievable financial goals that align with your long-term objectives. Whether you’re saving for a down payment on a house, paying off credit card debt, or building an emergency fund, CreditU can help you get there faster.

With features like spending and income tracking, personalized financial advice, and goal tracking, CreditU puts you in control of your finances and helps you achieve your financial dreams. So why wait? Download CreditU today and start taking control of your financial future!

Key Insights – Setting Financial Goals

1. Setting financial goals is akin to setting a GPS for your life’s journey. With a clear destination in mind and a roadmap in hand, you’re better equipped to navigate through financial decisions, big or small.

2. Start with the end in mind, break it down into actionable steps, and embark on your journey toward financial clarity and freedom.

3. Have clarity on your short, medium, and long-term financial goals. Plan accordingly and reach out for help when you need it.

4. Staying on top of your plans is the only way to see them through. Have the flexibility to change according to how the financial landscapes are changing.

Last Updated on January 11, 2024 by Dilini Dias Dahanayake